To know the content, we need to understand the title of this topic first. Cost-Volume-Profit Analysis is a process or to analyse how much the cost will be incurred for a certain volume in getting the desired profit from a production. Get it? Huh!

In simple terms.... for example, how many units we have to produce and how much money we have to pay to produce the units to get our targeted profit. Let's say, you produced 100 units of product X and of course you will know how much money you have to use to produce that product X. You will also know how much to sell and that will form your total revenue. Then compare the total revenue with the total cost of producing the product, you will then get your profit or loss from this transaction. From here, you can also find the break-even point in production. Hmmm...another term..break-even point...

Break-Even Point.

Simple explanation for the above term is...the point where you break! The point where you have no profit and no loss. Just ZERO. The total revenue equals with the total cost.

Total Revenue = Total Costs

TR = TC

(Selling Price x Units sold = Variable Cost + Fixed Cost)

I assumed you have already understood what are variable cost and fixed cost. If you don't, find those in this blog!

I give you an example... A fruit tart case

Selling price: RM4.00/unit

Units sold: 1000 units

Variable cost: RM1.50/unit

Fixed cost: RM2,500

The calculation is like this;

Total Revenue = Selling price x Units sold

= RM4.00 x 1,000 units

= RM4,000

Total Costs = Variable cost + Fixed cost

= (RM1.50 x 1,000 units) + RM2,500

= RM1,500 + RM2,500

= RM4,000

Therefore, TR=TC

There is no profit nor loss! That's why we called this Break-even point. With this price of RM4.00 per unit of fruit tart, you need to sell 1,000 units to cover the variable cost or fixed cost. If you sell more than 1,000 units, then you'll get profits. If you only managed to sell less than 1,000 units then you'll get a loss.

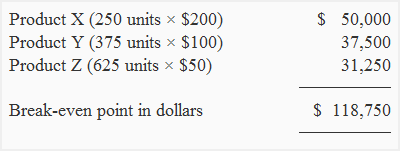

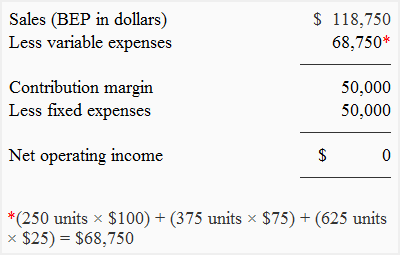

The above formula is a simple formula. There is another approach to arrive at the BEP.

Till next time!